In Canada

The concept of having your debts wiped out and starting again is very attractive, on the surface, at least.

The law has an escape clause that allows someone deep in debt to come out from underneath the weight of the obligation.

But there are some things you should know before you take that path.

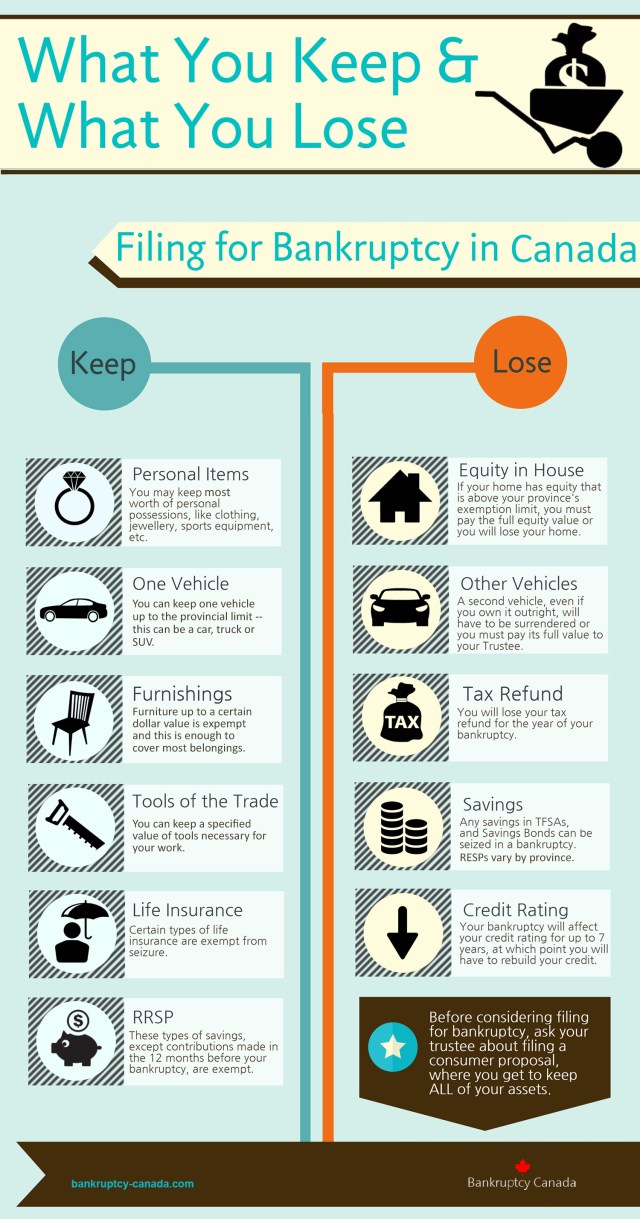

What you can keep and what you lose

Here’s a simple list of the wins and losses in claiming bankruptcy:

Total Debt Amount Defines Trustee Payments

After you keep track of your income versus expenses for six months, your Trustee in Bankruptcy will then define how much you need to contribute to your fund, and how long you need to pay that amount.

If your total debt load is minimal and there is no property to liquidate (summary), the payments will be expected for 9 months. If your debt load is larger (administrative), the timing is extended by 12 months, but only for first time bankrupts.

Should you not be someone who enjoys keeping a budget, the tracking of your income and expenses will seem like as big a task as anything you have ever done.

You sign a direct debit mandate from the agreement date, which will be adjusted after the six month review.

Behave Yourself

You will need to be a good person during the bankruptcy period. At the end of your specific term, your Trustee will apply for a discharge. If you’ve done anything foolish, finance-wise, during your term, the Trustee may seek to continue the process until he sees fit to apply again.

At the end of the term, the Trustee will total up the amounts you have paid into your fund, deduct his fees, and then share the residue among your creditors.

In most cases, the amount you pay into the fund will be swallowed up by the Trustee’s fee, so your creditors will come out with nothing at the end.

What Happens Then?

Well, in most cases, you will not be able to get back into debt for about five years. Can you imagine what that would be like? No credit cards, no overdrafts, no loans. Should you want to buy a home, you won’t even qualify for a mortgage. You will be a person without status.

In the USA

The laws in the United States have similar statutes, but you will need to consult a Bankruptcy Lawyer to discover what is involved.

Conclusion

This is a very serious step, so I would advise anyone thinking about it to be very sure it is what they want to do in the end. I have known people in positions of trust to be let go from their jobs when they applied for bankruptcy. (This is especially true if you work for a financial institution.)

A Consumer Proposal could be better in the end, but you will be paying for a longer period of time (five years), hopefully on a reduced debt load. However, your status will be impinged, all the same. Just saying.

Post Script

British Bankruptcy laws in the UK work along similar lines as the Canadian laws.